Evolving customer expectations and behaviour, regulatory frameworks, and emerging technologies are driving financial institutions to create and innovate solutions and services to meet and define the new normal. Open banking is a new paradigm in financial services that is revolutionizing the way we bank. It allows third-party providers (TPPs) to access consumer financial data from banks and other financial institutions using application programming interfaces (APIs), with the consent of the consumer.

The global open banking market size is expected to reach USD 135.17 billion by 2030, expanding at a CAGR of 27.2% from 2023 to 2030 In India, several factors are contributing to this growth: smartphone penetration, cheap internet access, willingness to adopt and adapt (online payments, e-commerce for example), government digitalization initiatives like Digital India, and the regulatory push to promote open banking.

Building Blocks of Open Banking in India Over Time

India’s foundational approach to public digital infrastructure led to the development of India Stack – a revolutionary digital stack comprising of open APIs and tools used to build a more efficient and transparent government and financial services ecosystem in India. Launched a decade ago with identity digitisation, grown to interoperable payment, India Stack is set to unlock the true potential of data with Open Banking.

Open Banking Applications in India

India has embraced open banking and introduced various applications that are revolutionizing the way financial services operate. A few noteworthy innovations are:

- CIBIL: India’s first credit bureau built using open banking technology, helping calculate credit scores widely used by banks and financial institutions

- Payment solutions: UPI is the most used open banking application in India, gained momentum after demonetization in 2016, and has made lives easier by connecting bank accounts, enabling users to carry out real-time transactions and payments

- Embedded Finance: Embedded finance is the integration of financial services into everyday products and platforms. Think in-app payments, peer-to-peer lending, micro-insurance such as travel insurance while booking your flight tickets.

- Central KYC: A single KYC repository that connects and verifies an individual’s identity with one click making KYC verification and modification easier and faster

The scale of the open infrastructures is immense; as of May 2023, UPI processed more than 9.4 billion transactions in a month, amounting to more than ₹14.89 lakh crore. These infrastructures extend the benefits across the value chain of financial services industry, including consumers, businesses, fintechs, banks, and other financial institutions.

For customers, it can provide greater control over their financial data, access to better financial services and even personalized financial products. For businesses, it can open new opportunities to reach and retain customers, improve risk management, ensure compliance, and provide better customer service.

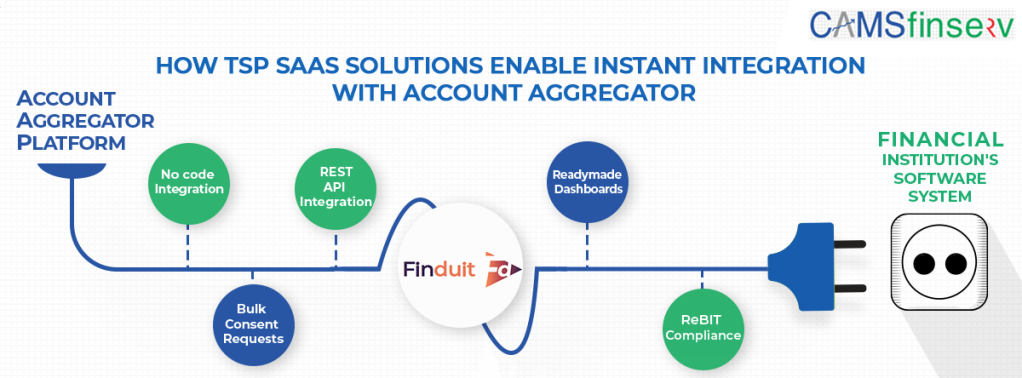

Data-Driven Account Aggregators: A Thriving Opportunity for Fintechs

Account aggregators help individuals securely and digitally access and share information from one institution holding financial information with any other regulated financial institution in the AA network. By making financial data sharing easier, more secure, and more cost-effective, account aggregators can help to create a more efficient and competitive financial services market.

Allowing consent-based flow of data may lead to the growth of new players across sectors such as lending, wealth management, personal finance management, robo-advisory, and even accounting. Moreover, it can usher in a new era of financial inclusion for the financially underserved, with India being the largest microfinance market globally.

Figure: Financial Information Sharing and Consent Process

Impact of Open Banking

- Hyper-personalization: Open banking can deliver diverse, timely, and accurate financial data that can be used to create tailored and relevant products and services, personalized to the unique needs of the customer. For instance, a TPP could use a consumer’s financial data to create a personalized budget or to recommend the right insurance cover.

- Sachet-solution for financial inclusion: Formal credit is inaccessible to the MSME sector due to a lack of the right documentation, inadequate collateral, outdated underwriting processes, and high transaction costs. Open banking can solve for these challenges and bring down the transaction cost of lending, investing, and insurance sales, while making sachet sales of lower ticket sizes profitable for businesses

- Banking 2.0 with improved customer experience: Consent-based, secure data movement can revolutionize the digital journeys of regulated entities. This means reduced operational costs and manual errors, improved ease of use, better customer service, reduced risks, new and innovative products and services.

- Anti-Money laundering: Instead of accessing only a fraction of customer financial data, institutions would be able to gain a broader view of the entities they’re doing business with. This would make banks and financial institutions better at detecting fraudulent behaviour and building early warning signals.

- Financial product innovation: Financial institutions can have access to consolidated data. Timely and reliable data inputs can help develop and innovate financial products and services. For example, a lender could use open banking data to develop a new credit scoring model that is more accurate than traditional credit scoring models.

Key Tenets of Open Banking

While open banking brings new and unique business opportunities, responsibility of creating a successful open banking ecosystem lies with all the stakeholders; from respecting the regulatory compliance to key consideration to adequate data privacy and cybersecurity measures. Successful implementation of the DEPA framework and AA architecture can help India become a data democratic society, embedding consent-granting mechanisms into data transactions, and making data interoperability a reality.

– Prateeksha Rawat

AVP, Marketing at CAMS

About CAMSfinserv

CAMS Financial Information Services Pvt. Ltd., is one of India’s first RBI licensed Account Aggregators. Headquartered in Chennai, the company is a subsidiary of technology-led financial infrastructure and services provider Computer Age Management Services Ltd., (CAMS). CAMS has been an integral part of the Indian Financial Services sector for over three decades providing platform-based services for Asset Management industry, Insurance companies, Pension & Account Aggregator and serves over 350 financial institutions in

the country. CAMS has ~69% market share serving Rs.28 Tn of the Rs.40 Tn MF industry. CAMS and its group companies are regulated by SEBI, IRDAI, PFRDA and RBI.

For more details, visit camsfinserv.com

{kind=link}